August 2025 Market Updates

The Share Market

August 2025 provided a compelling snapshot of the global investment climate, where cautious optimism continued to outweigh persistent economic concerns. For investors in both Australia and the United States, the month delivered positive returns, though the journey for each market revealed distinct characteristics. Australia’s ASX 200 enjoyed a confident and robust climb, largely driven by strong domestic fundamentals. In contrast, the US S&P 500 followed a path of quiet resilience, overcoming an early dip to finish with modest but reassuring gains. We break down the performance of each index, exploring the factors that shaped their movements.

ASX 200

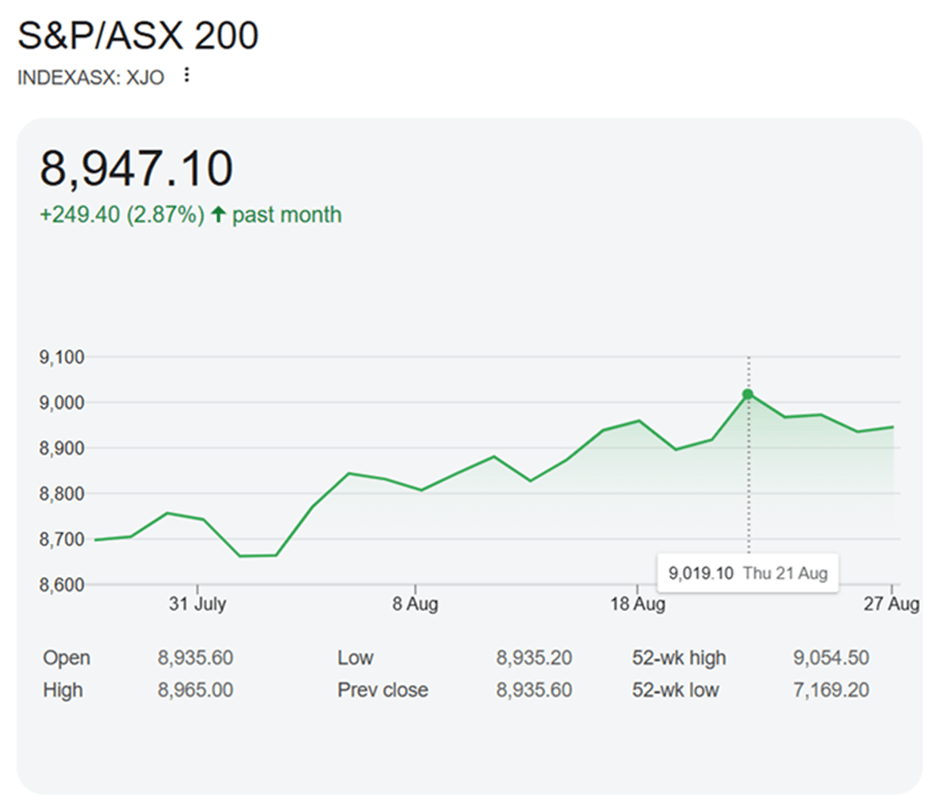

The S&P/ASX 200 exhibited a robust uptick through August 2025, giving investors cause for cautious optimism in the Australian equities market. As of 27 August, the index stood at 8,947.10, marking an impressive gain of 249.40 points or 2.87% across the past month. This period neatly encapsulates the dynamic nature of Australian shares, revealing both resilience and careful navigation in response to evolving local and global factors.

Source: Google Finance

August began with the ASX 200 sitting just below 8,700. The opening week was marked by subdued movements, as investors appeared reticent amid ongoing conversations about global inflation, shifting commodity prices, and the uncertain outlook for China’s economy — a major influence on Australia’s resource-heavy market. It wasn’t until after this quiet opening that the narrative began to shift, with the index dipping to its monthly low just under 8,700, reflecting some initial hesitance among traders.

The start of August saw something of a turnaround. Stability in local employment figures and stronger-than-expected earnings season updates for some major players created a mild flurry of buying, particularly among financial and resource stocks. This momentum built steadily through the month, lifting the ASX 200 well above 8,800 and approaching its best monthly levels. The peak came on 21 August, when the index reached 9,019.10—the highest point during the period. This surge was underpinned by confidence in domestic fundamentals, tempered only slightly by questions over longer-term global demand and policy signals.

Unlike some more dramatic run-ups, the ASX 200’s mid-month climb reflected layer upon layer of positive incremental news, especially from banks and miners. Enthusiastic investors pushed the market higher, responding to a blend of company results and macroeconomic signals that pointed to ongoing resilience in the face of broader international uncertainty. Foreign inflows into Australian shares further fuelled sentiment, contributing to the steady rise.

After hitting its high of 9,019.10, the index tapered somewhat, moving back towards the 8,900 range but remaining well supported. This gentle retracement is typical following a period of rapid ascent—some market participants will opt for profit-taking, while others sit back and reassess valuations in readiness for September’s trading. Importantly, the ASX 200 maintained a position substantially above its monthly low throughout, reinforcing the sense of underlying strength rather than fragility.

Minor fluctuations late in the month likely reflected both local profit-booking and responses to small global ripples, such as volatile commodity movements or changes in central bank commentary. The healthy difference between the month’s low (just under 8,700) and its high (9,019.10) confirms the market’s confidence, as well as the disciplined approach of most participants.

Investor behaviour in August reflected a shift towards yield, with anticipation of dividends from large resource firms and banks increasing activity in those stocks. Local company updates and regulatory news added to day-to-day volatility, but confidence remained strong as investors focused on sustained returns from leading Australian businesses.

Technical review of August shows the ASX 200 was buoyed by multiple catalysts. The lack of sharp corrections and the generally upward slope signal that sentiment, locally at least, favoured stability and progress. The wide gap to the 52-week low (7,169.20) underlines how far the market has come in a year, while proximity to the 52-week high (9,054.50) highlights the index’s remarkable recovery from previous lows.

Investors in Australian shares benefited from the graceful climb, with retracements proving mild and foreseeable. On balance, the market’s performance suggests superannuation balances and personal portfolios would have seen healthy gains for the month, helping counter inflation’s bite elsewhere.

S&P 500

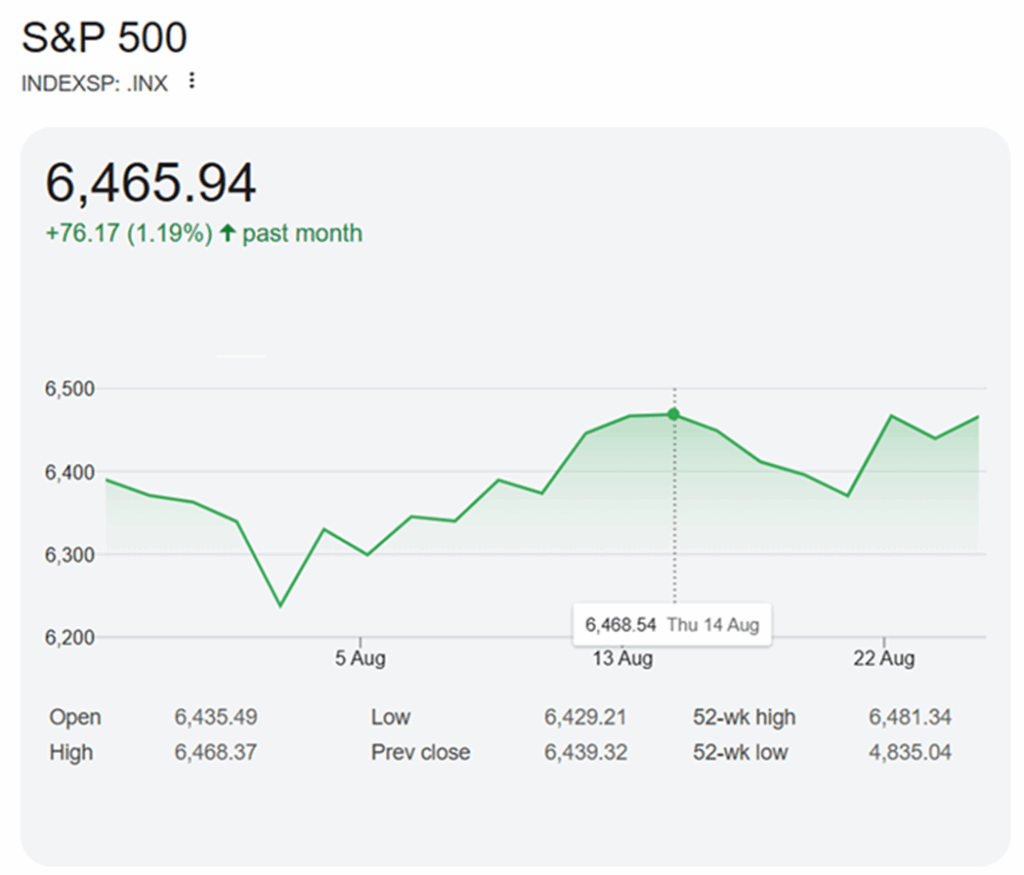

The S&P 500’s most recent month, spanning late July through late August 2025, showcased the index’s blend of stability and selective appetite for risk. By 26 August, it closed at 6,465.94—up 76.17 points, or 1.19% over the previous month. The graph documents a period shaped by several gentle shifts, rather than violent swings, giving an impression that US equities were being steered with a measured hand.

Source: Google Finance

The graph traces a decline in the S&P 500 through early August, bottoming out around 6,250 on about 5 August. This drop likely stemmed from investor caution in response to uneven economic data, including employment updates and consumer sentiment surveys that reignited debate about the US Federal Reserve’s next move. Despite the apparent unease, buyers emerged to support the market at lower levels, with renewed interest in technology and industrial stocks leading the rebound.

Rather than a sustained slump, the dip served as a buying opportunity for those confident in longer-term trends. The index recovered briskly, pushing back above 6,300 by mid-August, with sentiment stabilising as a result of strong company earnings and the absence of disruptive global events.

Mid-August saw the S&P 500 consolidate in the mid-6,400s, reaching a high of 6,468.54 around 13–14 August. Earnings season, particularly for large US multinationals, provided positive surprises, helping reinforce cautious optimism. Gains were broad-based, touching both growth sectors such as tech and steady stalwarts including healthcare and consumer staples.

There remained traces of nervousness — worries over interest rates, global politics, and supply chain issues lingered. But overall, much of the market was content to hold ground, reflecting faith in fundamental corporate strength and a belief that no sudden shock would upend recent gains.

As August unfolded, the index dipped briefly before rallying back towards its end-of-period high. Closing at 6,465.94, the S&P 500 had recaptured nearly all its mid-month strength, confirming positive sentiment among investors. The shallow nature of both dips and rallies hints at a well-balanced market, keen to avoid excessive risk but quick to capitalise on opportunities.

The actual monthly low rests near the 6,250 mark reached in early August, making clear that volatility remained present though contained. The strong recovery and measured upward trend provided reassurance for those watching for signs of fragility.

Running a technical lens over the S&P 500’s recent form, the month’s range — low around 6,250, high nearly 6,470—demonstrates steady progress and successful navigation of global uncertainties, at least in the short term. The index sits far above its 52-week low of 4,835.04, with the 52-week high at 6,481.34 almost matched during this period, suggesting ongoing investor faith in US corporate earnings.

Conclusion

Comparing the two indices, August was a story of different styles achieving similar positive outcomes. The S&P/ASX 200's performance was assertive, driven by the strength of the domestic economy and its key industries. The S&P 500's performance was more defensive, showcasing a quiet resilience and an ability to recover quickly from setbacks.

For everyday investors, these trends are encouraging. The strong showing on the ASX is welcome news for Australian superannuation balances. The stability of the S&P 500, meanwhile, provides a reassuring backdrop for the global economy. Together, they suggest that while challenges remain, investors are still finding compelling reasons to stay invested in quality companies on both sides of the Pacific

The Residential Property Market

Data recently released from Cotality's Home Value Index (HVI) reveals a continued upward momentum in Australian residential property values from July to August 2025. This broad-based growth reflects a mix of low housing supply, improving consumer confidence, and the easing of interest rates. Across the country, significant variation is evident between cities and regions, with some areas experiencing robust gains while others show more modest increases amid affordability challenges.

Overview of National Market Trends

Nationally, dwelling values rose by 0.6% in July 2025, marking six consecutive months of residential property growth. This consistent rise has been supported by factors such as persistently low housing inventory — around 19% below the five-year average — coupled with slightly higher sales activity, which is 1.9% above the average for this time of year. The combination of constrained supply and strong demand has led to auction clearance rates consistently above the decade average since mid-May.

Over the quarter ending July, national dwelling values increased by 1.8%, the strongest quarterly performance since mid-2024, while annual growth reached 3.7%. Houses have notably outperformed units, with house values rising 1.9% over three months (adding about $16,700 to the median home price), compared to a 1.4% lift for units. This divergence is attributed to a recovery in borrowing capacity for higher-income households, who tend to favour detached housing, and a shortage of new multi-unit developments.

Despite these positive trends, national housing affordability remains a significant restraint on price growth. The dwelling value-to-household income ratio remains near historic highs at 7.9, dampening broader market gains even as lending conditions improve with falling interest rates. Additionally, elevated household debt levels are subject to regulatory scrutiny, moderating rapid price escalations.

City-Specific Property Movements

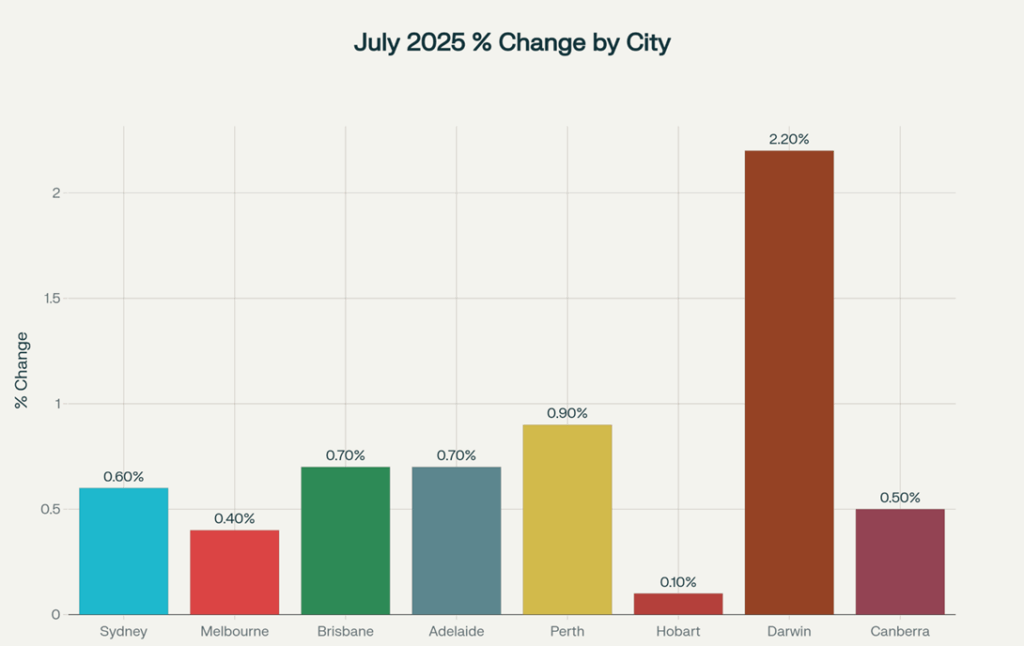

Across Australian capitals, every city recorded growth in dwelling values in July, though the pace varied considerably:

- Darwin surged ahead with the strongest monthly increase of 2.2%

Leading the growth, Darwin posted a notable 2.2% rise in dwelling values, indicating a particularly active housing market. This strong performance is reflective of increasing buyer interest and possibly economic factors or local developments that are boosting confidence in this northern capital. Darwin’s substantial gains highlight it as one of the standout markets in Australia at this time. - Perth followed with a robust 0.9% monthly gain

Perth’s property values also showed healthy growth, rising by 0.9% for the month. This is a significant acceleration for the city, marking the fastest pace of growth since September of the previous year. The boost in Perth’s market is likely fueled by improving economic conditions, infrastructure projects, and a renewed buyer appetite, positioning it as an important contributor to the national housing recovery. - Hobart recorded the slowest increase, rising just 0.1%

At the softer end of the spectrum, Hobart’s dwelling values edged up by a modest 0.1%. This minimal growth could be attributed to various factors such as market saturation, slower economic growth, or limited demand pressures compared to other capitals. Nonetheless, even this slight increase underscores a stable housing market, avoiding any price declines. - Brisbane and Adelaide saw solid growth of 0.7% each

Both Brisbane and Adelaide posted strong monthly gains of 0.7%, buoyed by increasing local demand and relatively better affordability compared to larger markets like Sydney and Melbourne. These cities are attracting buyers looking for more cost-effective housing options, supported by favourable local economic conditions and lifestyle factors, which continue to underpin their positive price momentum.

The combined capitals index rose 0.6% for the month, with quarterly growth at 1.8%, compared to combined regional areas’ 0.6% monthly and 1.7% quarterly growth. Notably, some regional markets in Victoria, Queensland, and South Australia exceeded their respective capital cities in quarterly growth rates.

Source: Cotality's Home Value Index (HVI)

Sydney’s dwelling values increased 0.6% in July, continuing a steady growth pattern, though annual gains remained modest at 1.6%. Melbourne posted softer monthly growth of 0.4%, reflecting lingering caution after previous market corrections. Conversely, Brisbane and Adelaide notably maintained stronger annual growth rates of 7.3% and 7.0%, respectively, driven by relative housing affordability and population growth dynamics.

Darwin’s remarkable 2.2% monthly uplift aligns with its 8.5% annual increase, highlighting its status as one of the hottest markets in Australia. Perth’s resurgence is evident in its 0.9% monthly rise and 6.5% annual growth, supported by economic recovery and infrastructure investments.

Regional Market Highlights

Regional Australian markets show robust performance, with annual gains of 5.9% compared to 3.0% for combined capitals. Specific regional centres such as those in Queensland, South Australia, and Victoria are leading growth outside major cities, fuelled by lifestyle changes, remote work policies, and relatively affordable housing options.

Top-ranked regional areas for dwelling value increases include Wheat Belt in Western Australia (21.9% annual growth), Maranoa in Queensland (18.5%), and the Outback regions of South Australia, where annual gains also exceeded 10%. This reflects a shift towards a broader geographic distribution of housing demand, beyond capital city hotspots.

Rental Market Developments

Alongside rising property values, the rental market has also tightened, with rental vacancy rates hovering near historic lows (1.7% nationally in July). After a period of subdued rental growth, rents across Sydney and other capitals have started to reaccelerate, with Darwin units posting the highest quarterly rental growth at 2.9%, and Hobart houses also experiencing strong increases.

Nationally, gross rental yields have slightly declined to 3.68%, yet remain relatively high in markets like Darwin (6.4%), reflecting favourable rental income relative to property prices in these areas. The widening gap between owner-occupied and rental affordability is placing increasing pressure on renters, particularly younger and lower-income households.

Outlook and Market Drivers

Looking ahead, the outlook for the Australian residential property market remains positive but measured. Cotality's forecasts point towards modest but broad-based price growth throughout the remainder of 2025. This is primarily supported by expected further interest rate cuts, easing inflation pressures, and ongoing low housing supply due to constrained new dwelling construction and rising building costs.

However, the market faces several headwinds including affordability constraints, regulatory limits on household borrowing, geopolitical uncertainties, and a moderating population growth rate. These factors may temper the pace of price increases, helping maintain a balanced market environment overall.

Lower interest rates could also spur stronger consumer sentiment and housing activity, historically linked with improved transactions and price movements. Yet, the shortfall in newly built homes is anticipated to persist for at least the next couple of years, underpinning continued supply pressures and supporting price resilience in established housing stock.

Inflation and Interest Rates

Australian inflation in August 2025 continues to moderate, stabilising within the Reserve Bank of Australia’s (RBA) target range of 2 to 3 percent. The annual inflation rate reached approximately 2.8 percent for the year to July, driven primarily by increases in housing, food, and alcohol prices. Notably, energy bill rebates have helped soften the impact of rising electricity costs, while slower growth in rents and insurance expenses has also contributed to the easing inflation trend. Consumer expectations around inflation have declined to about 3.9 percent, indicating growing confidence that price rises will remain under control in the near term.

This moderation is significant as it signals that the previous rounds of interest rate hikes have begun to have the desired effect on cooling the economy without triggering a sharp slowdown. The gradual return of inflation to within the target range is a positive sign for consumers and businesses, providing greater certainty around pricing and costs. However, some price pressures persist, particularly in energy and housing-related sectors, which remain closely watched by both policymakers and market participants.

In response to these developments, the RBA lowered the official cash rate by 25 basis points in August, bringing it down to 3.60 percent — the lowest level since April 2023. This move reflects confidence that inflation is returning to a sustainable level, while also aiming to bolster economic growth through increased household spending and business activity. However, the RBA remains cautious, closely monitoring uncertainties related to global trade and labour market conditions that could impact domestic economic momentum.

The interest rate cut is also intended to support an easing labour market, which has shown some signs of softening but remains reasonably resilient. With unemployment steady and wages growth still moderate, the bank’s cautious approach signals a balancing act between maintaining inflation targets and fostering employment growth. The RBA’s messaging has stressed that while the door is open for further easing, any future moves will depend heavily on incoming economic data.

Looking ahead, the major Australian banks are aligned with the view that further interest rate cuts are likely in the coming months. The country’s largest lenders — ANZ, Commonwealth Bank, National Australia Bank, and Westpac — anticipate at least one more 25 basis point cut by November 2025. Beyond this, National Australia Bank and Westpac project multiple additional reductions early next year, potentially lowering the cash rate to a range between 2.85 and 3.10 percent by mid-2026. While ANZ and Commonwealth Bank adopt a slightly more cautious stance, all agree that the overall trajectory points towards a gradual easing of monetary policy. Future decisions, however, will remain data-dependent, with the RBA poised to adjust its approach based on evolving inflation, employment, and economic growth indicators. This outlook paints a picture of an Australian economy moving towards price stability supported by accommodative monetary policy. The combination of moderating inflation and expected interest rate cuts is designed to sustain household consumption and economic recovery, all while maintaining vigilance against external risks and domestic uncertainties. As such, both policymakers and financial institutions appear committed to striking a careful balance as they steer the economy through the remainder of 2025 and into 2026.